Reverse Mortgage Alternatives in Australia

If you have been contemplating how to access the wealth you have built in your home, then you may have considered a reverse mortgage.

For many older Australians, a reverse mortgage has long been perceived as the best home equity release method when you are later in life.

But the reality is, they are not the only option and now there is a modern alternative for the over 55 cohort, which is also available to first-time borrowers aged 18 and above.

Discover more about why innovative solutions like the Midkey No Monthly Payments Loan might be better suited to your current financial circumstances.

How Do Reverse Mortgages Work?

You may already be researching reverse mortgage calculators, or know how this form of equity release works. If not, let’s quickly unpack how they are generally structured.

In broad strokes, a reverse mortgage allows you to borrow money against the equity in your home without having to make regular repayments.

The loan is normally repaid when you sell the property, move into aged care, or pass away.

For some retirees, this can provide access to funds for living expenses, medical bills, or lifestyle needs, on a progressive draw down basis while remaining in the family home.

A traditional reverse mortgage may be appealing, however reverse mortgage lenders have strict age-based Loan to Value Ratio (LVR) limits which can often be restrictive for younger borrowers. We will get into this in the next section.

If your application for a reverse mortgage has been declined, or you do not think it is the right fit for you, here are some reasons to consider a Midkey No Monthly Payments Loan for additional financial support.

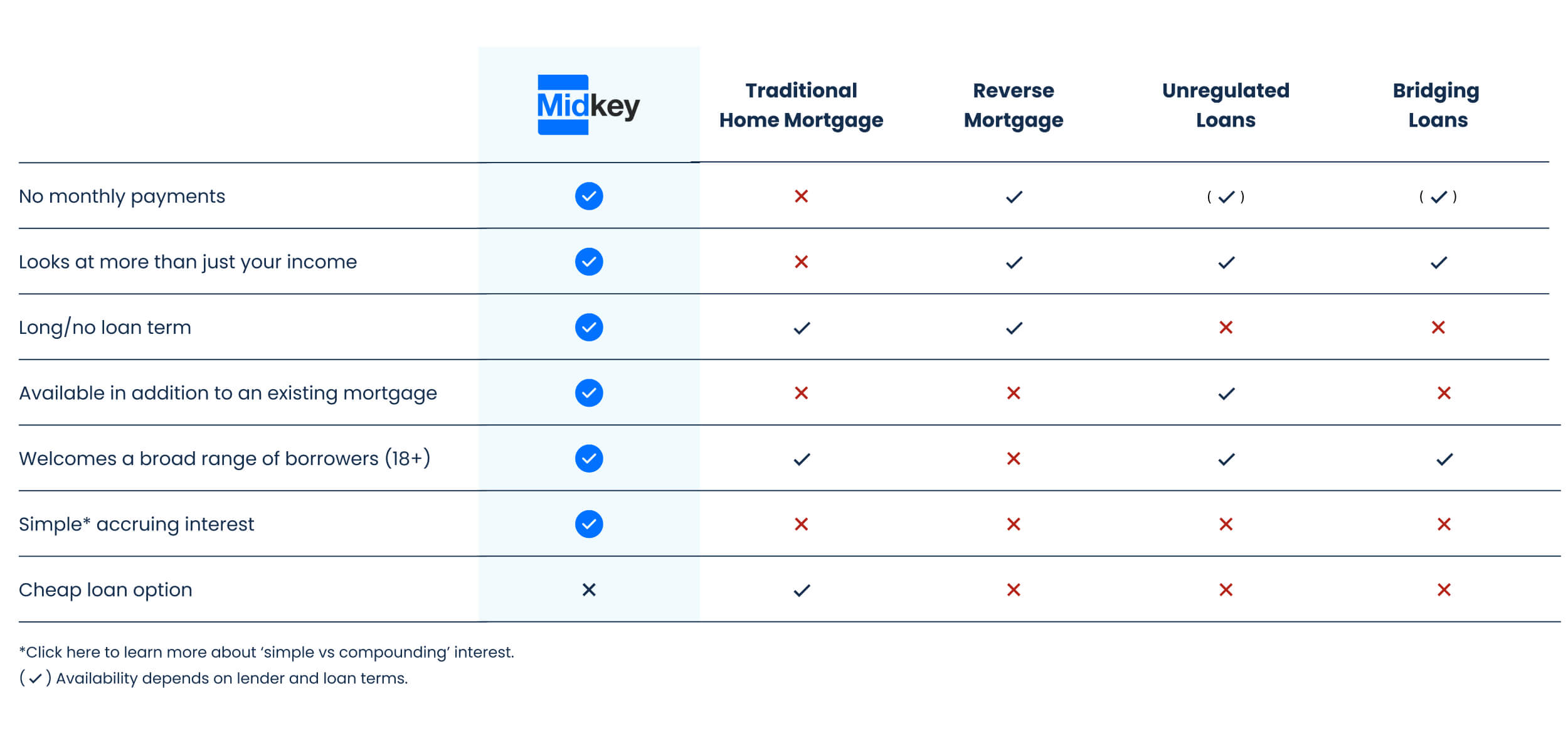

Traditional Reverse Mortgages vs Midkey: The Key Differences

A Midkey No Monthly Payments Loan and reverse mortgages share some similarities, however there are many important distinctions to understand.

Here are some of the aspects that differentiate the two funding options:

- Eligibility – Reverse mortgages are generally restricted to people over the age of 55, while Midkey is available to people of all ages (over 18).

- First or Second Mortgage – A Midkey No Monthly Payments Loan can be a first or second mortgage, whereas a traditional reverse mortgage is only available as a first mortgage. This provides more options for homeowners with an existing home loan, and you can use your Midkey funds however you want.

- LVR limits – Midkey can lend at higher Loan to Value Ratio limits. For borrowers aged 60, Midkey can lend up to a 35 per cent LVR, however a traditional reverse mortgage provider can only lend up to 20 per cent.

- Simple interest – Typical reverse mortgages accrue compounding interest at roughly two per cent higher than a Midkey No Monthly Payments Loan which has simple interest.

- Deferral fee – With Midkey, a Deferral Fee is only charged if your property increases in value above the Agreed Initial Value. If it does not increase, there is no Deferral Fee.

There are also other lending options available to you that come with their own unique sets of criteria and considerations. You can explore how these compare with Midkey below:

Before you decide to apply for a new loan, we strongly suggest consulting your financial advisor to ensure you understand how this will influence your financial position moving forward.

Why Midkey Is a Modern Equity Release Loan

If you are in your mid-life, planning for retirement, or have variable income that makes it difficult to meet traditional lending requirements, a reverse mortgage may not provide the flexibility you need.

Midkey was created by Australians for Australians to provide a more flexible and empowering loan option for responsible borrowers, offering a first-of-its-kind lending solution that can be structured as both a first mortgage or a second mortgage.

When used as a second mortgage, you can access up to 30 per cent of your home’s value. And you can obtain up to 35 per cent of your property’s value if you are debt free.

Simple interest accrues over the life of the loan (you decide when to repay) and the Deferral Fee mentioned earlier is paid at the end. This is a proportion of your home’s increase in value – if it does not go up, you do not pay a Deferral Fee.

Essentially, Midkey gives you the flexibility to access your home equity without being forced to sell, liquidate other investments, or take on more debt that adds to existing cashflow pressures.

Unlike reverse mortgages, Midkey does not just cater to retirement age borrowers that own their home outright. The Midkey model provides access to home equity for people planning their next strategic financial move.

Practical Uses For Your Midkey Loan

A Midkey No Monthly Payments Loan allows you to use your home equity to:

- Carry out renovations that enhance your lifestyle or increase your home’s value

- Provide financial support to help your children purchase their first property

- Cover education expenses, including private school fees

- Launch or grow a business, or ease the transition during a career change

- Offset the loss of income during maternity or paternity leave

- Finally take the dream holiday you have been planning for years

Explore Your Options with Midkey

Watch this explainer video to learn more about how the Midkey model works and who it is suitable for.

To see how much equity you could unlock, check your eligibility and try the Loan Calculator on our website.

Our experienced, Australian-based Loan Specialists are here to guide you through the process and answer your questions to help you determine whether a Midkey No Monthly Payments Loan is a good fit.

If you are ready to explore a smarter borrowing solution, connect with us today and take the first step towards using your hard-earned equity on your own terms.